Source: Solarbe

At the online press conference for the first quarter of 2022 held by the National Energy Administration, the relevant person in charge introduced that in 2021, the newly installed capacity of wind power and photovoltaic power generation in my country will exceed 100 million kilowatts, and the total installed capacity of renewable energy power generation will reach 1.063 billion kilowatts, accounting for 44.8% of the total installed power generation capacity, achieving a good start to the development of the "14th Five-Year Plan". Among them, photovoltaic power generation increased by 54.88 million kilowatts, which is the largest annual production in the past years, and continues to rank first in the world.

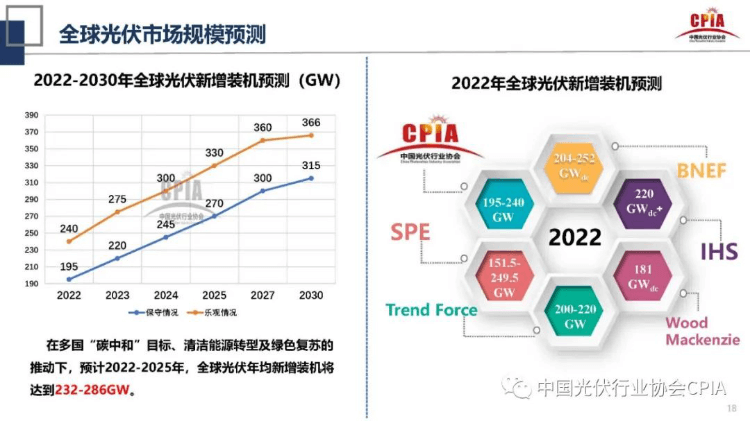

At the 2021 Development Review and 2022 Situation Outlook Online Seminar organized by the China Photovoltaic Industry Association yesterday, honorary chairman Wang Bohua gave optimistic expectations for the photovoltaic market prospects in 2022 in the report, and many institutions also gave domestic More than 75GW of newly installed capacity and more than 200GW of new global capacity are forecast. Considering that the "module-inverter capacity ratio" of photovoltaic power station projects is generally greater than 1, the annual demand for photovoltaic modules is likely to be more than 250GW, of which crystalline silicon modules are not less than 230GW.

So, can all links in the photovoltaic industry chain meet such demands? According to statistics from Solarbe Consulting, by the end of 2022, the effective production capacity of cells and modules will exceed 350GW, and the production capacity of silicon wafers may even reach 450GW. Even for the relatively scarce silicon material, the annual actual output + overseas imports can reach 850,000 ton, and is expected to meet the demand of nearly 300GW of modules. Obviously, the main industry chain will not become a restrictive factor for the development of the industry.

However, just as the shortage of glass in the second half of 2020 caught everyone off guard, in 2022, the auxiliary material link may still restrict the production of photovoltaic modules. The person in charge of the supply chain management of a module company said, "Since the third quarter of 2020, photovoltaic EVA resin has entered a state of shortage, and many leading film companies in China have issued price increase letters. During the '14th Five-Year Plan' period, with photovoltaic modules With the rapid increase in production capacity, domestic EVA film may be in short supply for a long time."

Regarding the supply and demand of EVA film, PV InfoLink pointed out in a report that the global demand for film particles in 2021 will be about 780,000 tons, while the supply of EVA is only about 730,000 tons. There is a gap of about 50,000 tons, which is mainly made up by POE particles. . In 2022, under the condition that the film weight is still 480mg/㎡, the global photovoltaic module production needs about 930,000 tons of EVA film and about 160,000 tons of POE. An analyst said that switching to photovoltaic materials after the new EVA resin device is put into production often requires a long modulation period, and photovoltaic materials with high EVA content cannot be continuously produced, which means that the scale release of photovoltaic-grade EVA resin production capacity is slow. The effective incremental supply is limited, and it is expected that the supply and demand pattern of film resin may continue in 2022. "As the diameter of the welding tape continues to decrease, the grammage of the film will show a downward trend in the future, but there is uncertainty in the promotion of SMBB technology, and the industry should be cautious when making relevant calculations."

According to industry experts, at present, with the development of photovoltaic and cable industries, foaming, wire and cable and photovoltaic film have become the main consumption areas of EVA downstream, accounting for 82%. Although the proportion of EVA film in the cost of photovoltaic modules is only about 5%, the quality of the film has a greater impact on the quality, life and power generation efficiency of photovoltaic modules. Some analysts pointed out that the annual growth rate of EVA particle demand during the "14th Five-Year Plan" period can reach 22%, maintaining a sustained growth trend. In the future, with the continuous advancement of "carbon neutrality", the demand for high-end EVA in the fields of photovoltaic film and wire and cable still has significant room for growth. It is no exaggeration to say that whoever can take the lead in starting production expansion and stably providing EVA film products to module companies will become the new "hidden champion".

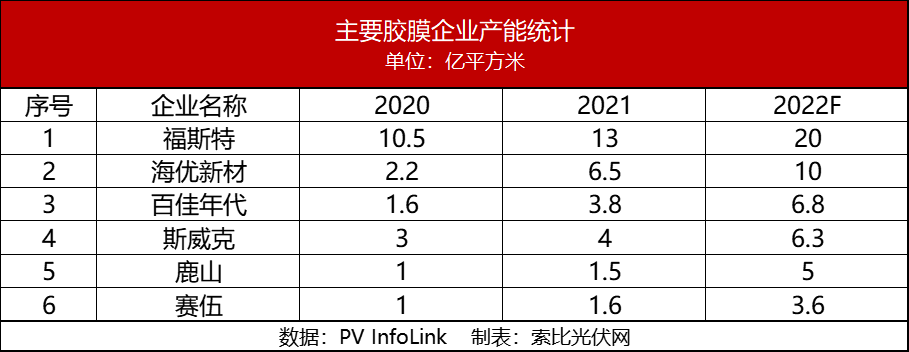

Solarbe Photovoltaic Network noticed that since 2021, leading film companies have successively released a lot of information on production expansion and production. Taking Changzhou Betterial as an example, the first phase of the 4GW project in the Vietnam base, the 8GW project in the Xianyang base, the 20GW project in the second phase of the Yancheng base, and the 20GW project in the Chuzhou base signed in January were successively constructed and put into production. According to an internal source, "the second phase of Betterial Vietnam base project is under construction. After the production is put into operation, the Vietnam base's production capacity will reach 16GW, and the total planned production capacity will reach nearly 100GW." Not long ago, Foster and Haiyou New Materials also stated that their The film production capacity will be increased by hundreds of millions of square meters, making preparations for the rapid development of the photovoltaic industry in advance.

To a certain extent, the actions of the above-mentioned leading film companies can alleviate the shortage of supply, but from the perspective of the industry as a whole, the supply and demand of photovoltaic film is still in a tight balance. According to PV InfoLink statistics, by the end of 2022, the nominal production capacity of plastic film (EVA+POE) can increase to more than 5 billion square meters, supporting the demand for modules above 500GW. Due to supply constraints, it is expected that the actual release rhythm of new production capacity will be significantly constrained. "Especially due to the short-term supply bottleneck of raw materials and limited actual market demand, the actual effective production capacity is very limited." The analyst said.

The ever-changing market conditions have brought great challenges to related companies. According to public information, Betterial shareholders list includes raw material suppliers such as Sinopec, as well as power station investment and development enterprises such as Three Gorges and State Power Investment Corporation. It can be said that the upstream and downstream of the supply chain are truly opened up. Analysts believe that as one of the earliest companies to develop and manufacture photovoltaic films, Betterial strategic layout in recent years can be described as very stable and sophisticated. On the one hand, we actively expand production to ensure that production capacity climbs steadily and consolidate our market position. On the other hand, we are not blind in the face of the influx of capital, and proactively choose high-quality capital cooperation. At the same time, we adopt equity cooperation and strategic cooperation in the supply chain. In this way, we can establish long-term and stable cooperative relations with large petrochemical enterprises at home and abroad. Under the background of the turbulent international situation and the sharp fluctuation of oil prices, it can significantly improve the security level of the supply chain, which is of great value.

A senior industry insider pointed out that judging from the clear photovoltaic installation plans in major markets, the demand for photovoltaic modules and EVA film in 2022 will be relatively rigid. It is expected that the price of EVA film will remain strong, and the profitability of film companies will be bullish. "In 2022, the price of upstream silicon materials and silicon wafers will enter a fluctuating downward range, which will greatly reduce the cost and price of photovoltaic modules, and drive the rapid growth of new installed capacity in the world, which will obviously stimulate the demand for EVA film by related companies." He emphasized, In 2022, under the premise of a tight balance between supply and demand, the performance and profits of major film companies will be improved to a higher level.